Please feel free to use this for your classes. Just acknowledge my name. Thanks!

Auctions:

I am going to concentrate on one topic rather than doing a survey of the extensive literature that exists for this topic. You can see that many types of auctions exist, look here:

There are many topics here that are of interest for both serious theoretical and empirical research:

What are the optimal bidding strategies for each type of auction? How does it depend on the information that the bidders have about a. the value of the item, b. the value that other sellers place on the item and c. the real-time bidding process of the auction?

How do prices in the auction market deviate (or not) from competitive prices or oligopoly prices?

What is the role of signaling in auction markets? How do bids convey information to other potential buyers?

We will look at only one problem:

Assume only one object is being auctioned. The format is sealed-bid first price auction, the winner gets the object and pays his bid “b”. If the value of the object to him is v, he gains v-b if he wins, and zero if he does not win.

If there are two bidders, and they value the same object v1 and v2 respectively, and if there is perfect information, and v1 > v2, bidder 1 would bid v2 + e, when e is a very small number and bidder 2 will bid v2. Of course 1 would win and have a gain of v1 – v2 .

The problem becomes interesting if we assume that there are two bidders, but they do not know each other’s valuations. Without losing generality, we assume that ti is valuation of type i, and ti is known to be uniformly distributed over [0,1].

In a Bayesian Nash equilibrium, what would be the equilibrium bidding strategy of ti ? This is the question we answer:

If ti wins by bidding b, he gets ti – b if his bid is higher than the other bid, otherwise he gets zero.

Therefore, ti’s expected profit from bidding an amount b is

Πi = (t-b) prob(bj < b)

We manipulate the term prob(bj < b) a little bit. Assume that a player with valuation t will have an equilibrium bid b*(t). Since the game is symmetric, both players will use the same bidding strategy in equilibrium. Further, the function b*(t) is monotonically increasing, which means higher t will induce a higher bid in equilibrium.

Therefore prob(bj < b) = prob(b*(tj) < b) = prob( tj < ϕ(b)) when ϕ(b) = inverse of b*(t).

But then prob( tj < ϕ(b)) = ∫ ϕ(b) xdx = ϕ(b), because of our assumption of uniform distribution of valuations.

So, in equilibrium, player “i” with valuation ti will maximize

Πi = (ti-b) prob(bj < b) = (t-b) ϕ(b), by choosing his bid b

Therefore the first order-condition, described below will be met for every t

∂ Πi /∂b = 0 = – ϕ(b) + (t-b) dϕ/db = 0

So, every t will bid according to above and in equilibrium every t will follow his equilibrium bidding strategy which implies that b= b*(t) or t = ϕ(b*)

Therefore, for any b* we will have

– ϕ(b*) + (ϕ(b*) –b*) dϕ(b*)/db = 0

Since every b* will satisfy the above, we may think of this as a simple differential equation in b

A note on differential equations:

Solution of a differential equation:

-y + (y-x)dy/dx = 0

Rewrite as

-ydx –xdy + y dy = 0

Or

(ydx + xdy) = ydy

Define a change of variables

Let z = xy, then dz = xdy + ydx

So we have, dz = ydy or taking integrals on both sides

z = y2/2 or xy = y2/2 or y = 2x (done)

Finally we apply this to get ϕ(b*) = 2b or b = ϕ(b*)/2

Or b*(t) = t/2

So every player, regardless of his own valuation, will bid half of his valuation in this game.

So, for example, expected profit of someone with valuation 75c will be

The biggest Ponzi schemer died in prison a couple of days ago. In case you do not know about him or maybe forgot, here is a short recap.

Madoff was a successful professional in the financial markets and ran his own trading business with his sons. On the side , he ran a brokerage business where he supposedly managed other people’s money. This is where he ran a Ponzi scheme which paid early investors with the funds supplied by new investors. Around 2008, when some large investors redeemed their portfolios, Madoff ran out of money and confessed to fraud. When the dust settled, it looked like the total amount the investors had was about 65 billion dollars, but this included the accumulated fictitious profits, so the actual amount invested and swindled was about 19 billion.

Madoff was sentenced to 150 years in prison where he died a few days ago. Madoff’s trustee, Picard and his law firm have recovered a lot of the original investment for the investors. The litigation mess that Madoff’s collapse started will likely go on for the next ten years.

Madoff was way smarter than me and possibly you , otherwise he could not have fooled so many people for so long. Very wealthy , highly educated people fell for his pitch as did sophisticated people working as money managers.

There are many reasons for this. The most prominent one is greed – since Madoff was well-known in the financial markets, lot of people assumed he has some secret strategy that he can use to generate steady returns every year. We teach in finance and economics courses that such strategies do not exist. If someone has a strategy like that, billions of dollars will be available to him for investment, which will lead to a breakdown of the financial system or a nullification of the said strategy.

In the history of the modern financial markets, some people have been able to generate extraordinary returns for a few years , but afterwards they all have closed their funds to new investors. Why? Because they themselves are not sure whether their strategies will continue to be successful .

The greed that I mentioned above was aggravated by second round fraudsters – these people were hedge fund managers who just dumped all their investors’ money to Madoff. Investors lost their money because of Madoff , and many of them sued these fraudsters for negligence, but they mostly weaseled out of these litigations claiming ignorance or simply a bad investment decision. Some of these secondary fraudsters (Ezra Merkin, Walter Noel and others) settled with investors and/ or Picard (the Madoff trustee) , but they still have retained many millions of dollars worth of assets. These people were real lowlife weasels, none of them were found criminally culpable. Apart from the fiscal judgments levied against them , they came out unscathed from this massive fraud – Madoff would not have been as successful if he did not receive massive amounts of hedge fund money from them.

Naivete or sometimes plain stupidity played another part in all this. In spite of the internet being around for many years and a lot of material being available to teach basic financial literacy , I have met people that are shockingly ignorant about the basics of financial markets. Let’s see what their thought processes are.

When you are sick, you go see a doctor who is a skilled medical professional. Give him his fees and He will give you medicine – your health will improve.

When your appliances need to be repaired, you call a skilled repairman, who will, for a fee, fix them.

By the same logic, when your wealth needs to be invested, you will call a professional money manager. For a fee, he will properly invest your money and get you a higher than average return.

The above statement is FALSE . What is true is the following:

When your wealth needs to be invested, you will call a professional money manager. For a fee, he will properly invest your money and get you an average return.

If you find a money manager who is offering you a higher than average return for a fee – do not believe him and do not invest your money with him, It is that simple.

Wait a minute – a doctor earns his fee for his valuable expertise about your body, a repairman gets his fee for his valuable expertise about your appliances, but a financial expert gets his fee for getting you only the average return?

You can get an average return on a bag of money by buying an index fund with it (if you don’t know how, you can learn from the internet in about five minutes!)

Sadly, this is true, which means you do not need a financial advisor to invest in the stock market if you only want the average return (which has been pretty good over the last 80 years – beats buying a term deposit!!). And no honest financial advisor will promise you an above average return! What they might do is to look for short term opportunities for you depending on your risk-tolerance. In other words, they will gamble for you for a fee!! As long as you agree to this, it is perfectly alright to gamble (take risks ) in the financial markets – indeed some people I know have become very wealthy by gambling successfully in the financial markets. Further, some financial advisors will look very hard to get you a tiny little advantage by buying a combination of products. Hypothetically, suppose a bond issued in your city by a educational institution gives a tax break for the residents of the city. If you buy this bond with other products so that you qualify for the tax break, maybe you will get a quarter point extra return above the average on your portfolio for the next three years. If such opportunities exist, along with tax havens in inheritance trusts or foreign countries if you have a lot of money, it is the job for honest financial advisors to find those and charge you a hefty fee if you want to structure your portfolio according to their suggestions.

If you want to take risks, the financial markets are a great place for it. You can always gamble on some obscure stock like “Google” was about twenty years ago and become very rich. You may also never get that winner stock and squander all your money in futile pursuit. The choice is yours, so are the rewards and failures.

Just do not give your money to an old Jewish uncle or any uncle who promises you an above average return by using a secret strategy, Send the money to me, I will double it in a couple of years (just kidding!!).

Did I ever gamble in the stock market? Did I lose big or win big? The details of what I did will remain a secret, but overall I came out a winner , mainly because I got lucky. Because of that I do not invest in the stock market any more. My luck will run out this time.

I am indebted to Dr. Nadeem Naqvi for some lively discussion which led to the first draft of our joint paper and for graciously allowing me to use the material from our joint paper. I am also indebted to Dilobar Kassymova for providing research assistance.

In my classes, I sometimes show off different categories of economists (boasting that economists are not all dull and/or socially awkward!). I show them handsome economists (yes, they do exist!) athletic economists, superrich economists, transgender economists and many others. The most fun I have is when I show them a “clueless economist”!

Let me explain !

In mid 1990’s, a young researcher from Princeton wanted to test whether competitive markets in real life exhibit a uniform price (Graddy (1995)). She picked New York’s Fulton Fish market – a large wholesale fish market – selling mainly to restaurateurs and grocery stores, where a large number of independent stores operated from the same premises. Collecting a lot of data on sale prices and quantities and running several statistical tests, she found that the prices overall are the same for the same quality of fish. A little annoying item was that she found one ethnic group, Asians (and Koreans in particular), who were systematically discriminated favorably, meaning they usually paid a lower price than others!

It was a competent piece of research. However, the FBI took a keen interest in her research , they were already investigating Fulton Fish Market for collusion and other organized crime related activities! A little later the FBI accused the sellers of collusion, and soon afterwards the entire fish market mysteriously burned down, with all their records totally charred! (NYtimes (1995))

The reality, as I see it now, was that all the wholesalers were tightly controlled by organized crime, prices were not competitive but reflected almost perfect collusion, and the unfortunate Asians (Koreans) that bought cheaper fish were owners of inner city grocery stores in NYC area – they were paying protection money to the aforementioned organized crime group – so they got a little break on the fish prices!

I am sure the reality became obvious after the market burned down in 1996. Indeed, she mentions the involvement of organized crime in her later writings. And of course, I would speculate that she was not totally unaware of this at the time the data were collected and the paper was written (circa. 1991-93). But only the Federal Bureau of Investigation had inside information on this, not an academic economist.

Indeed, even in a market economy, sometimes things appear to be very different from what they really are.

When applying game theory to analyze equilibria in a more complex economy, the possibility of appearing to be clueless is a lot more serious. In a subgame perfect equilibrium, credible threats are usually not executed, so one might construct an incorrect hypothesis where credible threats are absent altogether. In political economy, where complex social and economic interactions are studied, one usually finds policy makers and academics who are blissfully naïve (and clueless)

My colleague, Nadeem Naqvi and myself have been perplexed by the “Stans” – we have been working in one of them for the last few years. On the surface, these “Stans” and other off-shoots of the Soviet republic are doing fine. Some have more resources than others. The BANK and the FUND periodically publish research monographs about foreign investment, business environment, GDP growth and other key economic indicators – assuming, erroneously, that these are budding capitalist economies. There is a steady stream of econometric work trying to predict efficiency of different monetary policy instruments and fiscal stimuli to promote economic growth

But the reality is, these are all “network” states, the “network” being a combination of government officials and others in power. Fiscal and monetary policies have superficial, at best marginal effectiveness in these countries.

The network state collects tributes legally by taxation and illegally by other means from business enterprises. They wield the threat of confiscation or loss of services. In return they provide order which is a combination of infrastructure and protective services. These are the important instruments, not traditional economic policy!

However, the “Stans” are not collapsing en masse, like the Soviet Union did. Indeed, some “Stans” are doing better than others. Some exhibit moderately high rates of growth and considerable private investment and business activity, whereas others only have the basic retail and other non-traded goods provided by the private sectors ! Is it because of their resource base? Or is it an outcome of a more complex game? Clueless we might be, but since we know some game theory, we tried to build a theory of “Stans” to show why some of them are more vigorous than others.

A little background here:

In the 70-year lifetime of the Soviet Union (1922-91), (i) there were virtually no property rights by which individuals had to live, largely because there was extremely limited private ownership of property (beyond one’s own autonomous labor), (ii) other than sale of labor time (hours or days for which labor power was sold), all other sources of income for a household were effectively prohibited, (iii) there were no businesses that households could buy and sell, nor of course any stock markets in shares of private firms, and (iv) there was no developed real estate market.

This was radically different from the economic base (of the relations of productionand the associated inter-household distribution of income) on which the capitalist economic systems of the world were organized at the time. Moreover, resting on this economic base in the Soviet Union, the entailed legal and political superstructures pertaining to individual rights over property were virtually nonexistent. This is a huge contrast with the successful capitalist countries, in which the legal structure dealing with property rights was firmly in place, and there were political institutions that collectively were in continuing support of such rights under the law.

By 1991, there was rebirth of fifteen post-Soviet countries, and in these the corresponding collective consciousness of the people was nothing like that in the successful capitalist countries.

What kind of progress have the Group of 15 made towards the state’s provision of greater protection of property rights of individuals, especially to the businesses they give birth to and nurture into successful and profitable enterprises, simply because the greater such protection, the more fertile (profitable) will be the domain of the economy over which private business investment will be made in larger magnitudes, and in higher-return ventures? The larger the annual private business investment, the faster is the rate of growth of the economy’s capital stock, to which corresponds a faster rate of growth of real GDP. To avoid the fate of the late Soviet Union, these countries must adopt a path of economic growth supported by private investment. The data available in these countries are not entirely reliable, the data on private sector capital formation is not available for some, in others it fluctuates wildly. Further, sometimes the network state embarks on a “prestige” project and private investment occurs as an ancillary to this project. Once the project is completed, private investment goes down substantially.

A snapshot of the Group of fifteen, 2016

GDP Per Capita

Gross fixed capital formation, private sector (% of GDP)

GFCF as % of GDP

Country Name

GDP per capita 2016 ($)

2012

2013

Lithuania

29972

Not available

Not available

Estonia

29313

Not available

Not available

Russian Federation

26490

17.6

18.5

Latvia

25410

Not available

Not available

Kazakhstan

25145

25.7 (in 2006)

not available

Belarus

18000

30.1

32.6

Turkmenistan

17485

10.5

not available

Azerbaijan

17439

11.8 (in 2007)

Not available

Georgia

10044

17.5

16.9

Armenia

8621

22.2

19.4

Ukraine

8305

17.2 (in 2009)

not available

Uzbekistan

6563

17.5

18.0

Moldova

5328

22.6 (in 2006)

Not available

Kyrgyz Republic

3521

24.1

22.9

Tajikistan

3008

4.0

5.5

Data on GDP and GFCF from various UN publications

It is clear that in terms of GDP per capita, some of these countries have performed a lot better than others. The data on Gross private capital formation is not satisfactory, but again we can see a large difference in these numbers between the group of fifteen. Several other countries in East Europe, Asia and Africa, may also satisfy our criterion of network states.

Gross capital formation as a percentage of GDP varies wildly, ranging from 4% in Tajikistan to about 30% in Belaraus and 25% in Kazakhstan. (for comparison , GFCF is about 15% in USA which has a very large capital base, but it is about 40% in China and 25% in India) Why is it that some network states are more successful in promoting private investment than others. Is it only because they have more natural resources. Or is the reality more complex?

We applied a little bit of agency theory to look at a game between the “network” state and the agents who may be “qualified” or unqualified”

2. Model

The government (network) provides legal order S and collects revenue (tribute) T. Order includes infrastructure for enterprises plus a threat level for confiscation. This is essential for collection of tribute.

To sustain high return enterprises, the government must provide an order level sH while the level of order needed for a low-return enterprise is sL. There are two types of agents:

“Qualified” – who either possess human capital or resources or have enough “network” connections to operate high return enterprises. They earn more from high return enterprises

2. “Unqualified” who earn more from operating low-return enterprises.

An unqualified agent may not be interested in operating a high-return enterprise, whereas a qualified agent has a choice of operating either a high-return or a low-return enterprise.

The objective of my exercise is to see under what conditions the equilibrium outcome will involve a situation where both high and low return enterprises are operated by the agents in the economy. This equilibrium is called a “productive” equilibrium. The other equilibrium is called a “stagnant” equilibrium because only low-return enterprises exist here, operated by both qualified and unqualified agents.

The payoff (surplus) from operating a high return enterprise by a qualified individual is

V = max [U(θ, S ) – T]

Where θ is the agent type (θQ qualified, and θU unqualified), sL is the order provided to low-return enterprises and sH is the order provided to high-return enterprises, and T is the tribute that must be paid to the government (tL to operate a low-return business, and tH to operate a high-return business).

Thus, if a qualified agent participates in a high return enterprise, his return is

VQH = U(θQ , sH) – tH

If he participates in a low return enterprise, his return is

VQL = U(θQ, sL) – tL,

Therefore he will choose to invest in H if VQH > VQL , and in L otherwise.

An unqualified agent, I assume, has a very low (possibly negative) return from investing in a high quality enterprise, so his return from investing in L is

VUL= U(θU, sL) – tL,

He will invest if VUL is non negative.

The main point of distinction between qualified and unqualified agents is

U(θQ, sH) – U(θQ, sL) > U(θU, sH) – U(θU, sL),

which implies that the qualified agents have a higher differential payoff between high return and low return enterprises.

The government maximizes a convex combination of the cost of providing order and the revenue earned,

G = – a[C(sL) + C (sH)] + (1- a)(tL + tH)

where a is the weight placed on the costs. Here G is the government’s objective function.

By assumption, it is more expensive to provide sH because it needs better infrastructure and possibly higher level of coercion so that greater revenue could be generated from the high return enterprises.

2. Equilibria

We look at three possible equilibria (scenarios). The proofs are in my joint paper with Professor Naqvi (Bhattacharya and Naqvi (2017))

1. The government provides only sL, enough to sustain low-return enterprise only. It is not profitable for the government here to provide sH, the revenue generated is the entire surplus of the agents (or the minimum surplus if the unqualified agents are diverse). This is the stagnant equilibrium. Here, the government does not find it optimal to provide sH because qualified agents will continue to choose low-return enterprises because for them the additional net return from operating higher return enterprises is negative.

2. The government provides both sL and sH, and collects different revenues tL and tH from different agents. Here, qualified agents choose high-return enterprises and unqualified agents choose low-return enterprises. The revenue earned tL is equal to the surplus of the unqualified agents – thus the unqualified agents are left with what we call only “normal profits”. The revenue earned tH from the high-return sector is less than the surplus of the qualified agents, because they self-select to operate high-return enterprises. So the qualified agents earn more than “normal profits”. This is the productive equilibrium.

3. The third scenario occurs where the government provides only sH and extracts all the surplus by collecting tH. Here, the low-return enterprises are not functional. We call this a “Highly-productive” equilibrium. This type of equilibrium will not exist if there is a large number of unqualified agents in the economy, or if it is not expensive for the government to provide order level sH. Thus, this is the kind of equilibrium that a society should strive for under improved governance and availability of opportunities.

For the kind of economies we are considering here, this equilibrium is unlikely to exist because there is likely to be a large number of unqualified agents who will find operating a low-return enterprise profitable even if their surplus is close to zero.

3. Remarks

1. What exactly happens in “stagnant” equilibrium?

This equilibrium is achieved as an outcome of voluntary interaction between a government which provides order and infrastructure and agents who decide to operate enterprises that they find profitable. In this equilibrium, although there are many qualified agents, they self-select to operate low return enterprises because the return from doing so is higher than operating high return enterprises. The government provides only order level sL because provision of sH is redundant in this case.

2. What exactly happens in “productive equilibrium”?

When is the productive equilibrium likely to exist? In a productive equilibrium, qualified agents operate high-return enterprises and unqualified agents operate low-return enterprises. Naturally, the level of private investment will be higher in this equilibrium.

I have proved that this equilibrium will exist when the proportion of qualified agents is neither too small nor too large. As we mentioned before, it is unlikely to be too large, so “not too small” is the relevant criterion. This proportion depends on the level of human and natural resources at the disposal of the agents and size and strength of the “network” in the economy

The second result I prove is that the productive equilibrium will exist when going from low to high order level increases surplus proportionally more for qualified than for unqualified agents.

4. More Remarks

We observe, in Central Asia, Eastern Europe, in south Asia and in Africa, different kinds or regimes where appropriation is the norm – both regimes with relatively vigorous economic activity and regimes with relative stagnation. This formulation might shed some light on why some regimes appear to be more stifling than others.

Did I just present you with a well-disguised tautology? Possibly!

So let me check again – what exactly is the implication of all this?

Basically, even in a network society, agents do not curl up and surrender all surplus to the network. Nor does the network brutally destroy the society. The outcome depends on the proportion of agents who are educated, connected to the network, and willing to take the risk of eventual confiscation of appropriation of their entire investment. If enough of these agents exist, and the network finds it not too expensive to provide the right infrastructure for high return enterprises, then the economy will exhibit a productive equilibrium where substantial private investment may occur. On the other hand, if this proportion is small, the network state will only build an infrastructure to support low-return enterprises. In a country like Tajikistan, for instance, private investment and economic activity are on a much subdued level than the relatively successful “Stans”. Each of the countries in this group has a varying amount of natural resources that they can export. But for sustainable growth, they all need development of vigorous economic activity. My model indicates that the proportion of qualified agents, and the “network’s” willingness to provide a higher level of infrastructure and property rights are some of the key elements for sustainable growth.

REFERENCES

Bhattacharya, G. and N. Naqvi, (2017), “A Theory of Appropriation under Self-selection by Agents” Mimeo. KIMEP University, Almaty, Kazakhstan.

Graddy, Katherine (1995), “Testing for Imperfect Competition at the Fulton Fish Market”, The RAND Journal of Economics, Vol. 26, No. 1 (Spring, 1995), pp. 75-92

3.Fire Sweeps Through Major Building at Fulton Fish Market

This year’s Economics Nobel was awarded to Milgrom and Wilson. Notwithstanding their characterizations by media as contributors to auction theory, both of them primarily worked in pure and applied game theory. Auction theory is actually an application of games, Milgrom found solutions for some very peculiar and exotic auctions , for example, auction of Radio frequencies to private companies. This was a very original application because of the unusual object being auctioned (air) and the difficulty of designing an efficient auction mechanism to maximize the gain to the auctioneer(the government).

Regardless of their contributions to auction theory, I want to point out how game theory evolved over time and what started as a very promising approach to analyzing human behavior turned out to have severe limitations – not because not enough research was done, but on the contrary a lot of research was done by some very brilliant people (including Milgrom!)

This could be illustrated perhaps by discussing Milgrom and Roberts (not Wilson) 1982 paper in Econometrica. Milgrom is not a lucid writer of articles, nor are most of the theoretical economists in our time. So I really started teaching from the article from early 1990’s possibly because I did not quite understand it before that time.

Let’s take one small part of the US antitrust Law and show how game theory evolved and policy changed over time

The Law simply says prevention of entry of new firms by charging a lower price (the technical term is limit-pricing) is illegal ( this is different from predatory –pricing where an incumbent firm charges price below cost to prevent entry – that is a more serious accusation)

Pre-game theory: Anytime a large corporation lowered price substantially, someone would accuse it of limit-pricing. Indeed, companies like Amazon could not have possibly survived during those times. (1950’s/60’s) The Justice department would have busted them open!

Post Game theory – initial stage – Research on entry games revealed that limit-pricing can not possibly be part of a subgame –perfect equilibrium. In fact, the threat of limit-pricing is not credible , because should entry occur, the incumbent firms will then concede entry because it is always more profitable to do so. In a marriage when one spouse is weak, the other one knowingly cheats because divorce is not a credible threat on the part of the weak spouse. So, even for large corporations (who play the role of weak spouses here), preventing entry by lowering price for the entire market loses more money rather than allowing entry of new firms and co-existing with them.

In the light of what I said above, if we observe a large incumbent company lowering price, it is because it has a better technology and it wants to capture the market by exploiting its superior technology. So, Amazon.com or Alibaba.com does not try to kick out other retailers, it succeeds to capture the market by being the most efficient selling portal on the internet . Whether its actions are socially justifiable, ethical, etc, is another story.

So, the policy of the government regarding enforcement of Anti-trust Law was changed sometime in late 1970’s. Technically, limit –pricing was still illegal, but practically it was much harder to prove, because an incumbent firm will always claim to have better technology. Anti-trust law was applied more to other non-price actions like creating effective entry barriers . IBM and AT&T were broken up during these times in massive anti-trust cases, but none were accused of limit-pricing.

Post-Game Theory –Later stage

Milgrom and Roberts took the entry game analysis one step further. They introduced two possible avatars of incumbent firms – one high cost and one low-cost (with a better technology) . They argued that if the entering firm does not know which avatar it is playing against, then the high-cost firm can mimic the low cost firm and charge the low cost firm’s price. Depending on the possible scenarios of losses and profits (which is quite complex), there could be an equilibrium where high cost avatar successfully mimics the low cost avatar, the low-cost avatar concedes the mimicry (because it costs him more not to) and the entrant does not enter because if it does, then, the probability of the avatar being low cost and the consequent loss is greater than just not entering at all!

So we can have successful limit-pricing under incomplete information! But then the Anti-trust policy now becomes much more complex, every single situation has to be investigated carefully to see if limit-pricing has occurred, or it is the low-cost firm selling at its normal price. A bonanza for anti-trust economists who got rich from 1990-2010 because every case became more and more complex. Economists’ testimony on both sides of a case often involved complex game theory models and supporting data and/or refutation of the other side’s models and data. Millions of dollars were earned during this time in consultant fees. Some of my friends/colleagues got rich, and I am sure Milgrom himself availed of these opportunities sometime during his distinguished career.

A lot of extensions were done on Milgrom and Roberts’ paper , of course, opening up even more complex scenarios about when limit-pricing can happen.

So as more complex games were solved successfully by people like Milgrom (and not so successfully by people like me), it ultimately became clear that in a complex game with super-sophisticated players, the set of equilibria is too rich – which means we can not build a policy framework based on game theory .

Milgrom and others wrtote a lot of papers on firm behavior that was applied to all aspects of antitrust and government regulatory agency problems. In fact, the limit-pricing result is only one of many significant contributions of Milgrom, used by me for illustration here.

Pretty much this is where it stands in the entire field of anti-trust nowadays. The economics consultants in each antitrust case or mergers and acquisitions case make a boatload of money on each side

As game theory has been too successful , it still helps us to understand the basic issues, but does not provide enough guidance for complex situations – besides indicating that many things can happen with sophisticated players under an environment of incomplete information! – which is something we knew already before all this began sixty years ago hahaha!!

Well, at least we micro people do not make consistently wrong predictions like some, (not all) monetary policy guys. But, I was hoping we could do maybe a little better!!

By the way, this comment does not even come close to an evaluation of Milgrom’s scholastic works which are far broader in scope than antitrust policies. Please see the link below:

Although the first paper on network issues was written by Rohlfs in 1974, network goods (or services) have become a very important part of most advanced economies .

What follows is my first lecture on “Network Services”, used frequently in Industrial Organization Courses

What is the difference between an ordinary service, say a haircut and a network service, for instance telephone service?

Haircut (only I look ugly as before!!)

The consumer who is getting a haircut gains utility from it, hopefully, and no one else is affected. But the utility one gets from having a phone depends on how many other people have telephones. So one consumer’s utility depends on the total number of buyers of the service.

Networking!!

We will discuss two market structures, monopoly and duopoly in the network market, also compare this with the social optimum solution. As we will see, the nature of equilibrium is substantially different from non-network goods.

First we derive the demand curve of a network service. Unlike non-network goods and services, the demand curve is not negatively sloped! This changes the nature of equilibrium.

Assume that consumers pay a single price p for accessing the network , but there is no charge for subsequent pay per use.

N is potentially the maximum number of consumers that may want to subscribe to the network.

Let vi be the value that consumer “i” places on the network when everyone subscribes to the network. In other words, vi is the maximum amount that “i” will pay for the network.

If all consumers are identical, then this is an easy model to analyze, but that is not a realistic assumption. So we assume that customers are different. They are distributed uniformly over the interval [0,100].

So, if the consumer knows that f is the fraction of total consumers subscribing to the network, the maximum that consumer “i” would pay is a function of f and vi. For simplicity, we assume that the consumer “i” will pay f.vi.

Therefore given a price p, there will be a consumer whose willingness to pay is vi^ such that

The price p = f vi^.

By our assumption of uniform distribution, the fraction of consumers who want to subscribe to this service is 1 – f = vi^/100

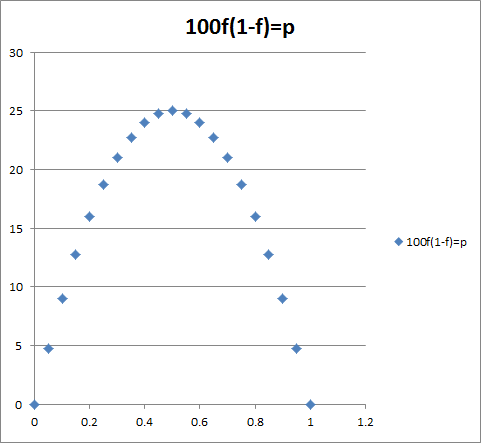

Therefore p = 100f(1-f) after a little algebra

This is the demand curve for network services, note that this is inverse demand showing p as a function of f, when f is the fraction of the total subscribing to the network.

“f” is fraction of people in the network

p is demand price

0

0

0.1

9

0.2

16

0.3

21

0.4

24

0.5

25

0.6

24

0.7

21

0.8

16

This demand curve is not negatively sloped.

It is positively sloped for f < ½ , reaching a maximum at p = 25.

Over the positively sloped range, some consumers quit (f falls), there are two effects:

Due to the price effect, demand price goes up (the people who would want to pay higher price would remain in the market)

Due to the network effect, the value of the network falls to existing customers, so some others quit as well.

As the network effect dominates the price effect over this range, as f falls, demand price p also falls

Over the negatively sloped range, the network effect is small because f is large, and the demand curve is negatively sloped.

Assuming Q = fN, we get the total revenue curve as

Q = pfN = 100f(1-f)fN = 100f2N – 100f3N

Network monopoly with marginal cost of 11.11 (no fixed costs)

My numbers are a little different from the ones in text , pages 642-3.

Π = pfN – (11.11)fN

= 100f(1-f).fN -11.11fN

Differentiating with respect to f, and setting to zero

100f(2-3f)N-11.11N = 0

Or

2f – 3f2 – 11.11/100 = 0

Or 3f2 -2f + (1/9) = 0

The solution is

Optimal f* = 1/6 {2 ±( 4 – 4x2x(1/9)}1/2

Which comes to f* = 0.6, p* = 24, and profit per-unit as 13.49

Total profit is 13.49N

We try zero marginal cost next

Π = pfN

= 100f(1-f).fN

Check the solution is f = 2/3, p = 100(2/3)(1/3) = 22.22

Profit per-unit is 22.22 (2/3) N = 14.8N

If price is zero, then everyone subscribes, total demand is N

The total social surplus is 1/6 N

The government may supply this for free and charge a tax per user of 1/6 ?

The other problem is how a network is built over time. In regular market as a price is announced, there could be a fraction of the total number of buyers at first, but the rest would come over time.

In a network market, a fraction of buyers may come initially, but if f is less than the breakeven point, the network may collapse if some decide to leave.

Network duopoly with Marginal cost 11.11

There is a Bertrand solution with price = 11.11.

But there is also another Nash equilibrium where one sells at the monopoly price and the other sells at 11.11 with zero customers. Because of the network externality, the firm with price 11.11 will not get any customers, if the monopoly is there first.

Interestingly, entry is also not possible here if there is a monopoly. One way to enter would be a dynamic strategy where the entrant offers it at a zero price, at a loss. Then the incumbent will either offer a zero price or exit. If the incumbent offers a zero price, they can both increase their price to 11.11 and make normal profits.

Alternately, because of network externality, any initial provider should provide the service at well below cost or for free and charge a one-time sign up fee. This would establish a large network, and new entry would be blocked since cost per period for the consumers is zero.

Lastly we generalize the monopoly model with and without fixed cost with the assumption that the consumers’ willingness to pay is uniformly distributed on an interval [0,K]. Here

Behind the first door, there are three dollar bills, behind the second door, there are five dollar bills, and behind the third door there are seven dollar bills. Players know about this.

Player 1 moves first. He can open any door and remove as many dollar bills as he likes from behind that door. Player 2 moves next. He can select any door, open it and remove as many dollar bills as he likes from behind that door.

The game continues, until there is only one dollar bill left. The player who picks up the last dollar bill gets zero, the other player gets all the money.

Remember, when it is your turn to play, you can open any door, but can not open two doors! After you open any door, you would have to remove at least one dollar bill from behind that door! And when it is your turn to play, you can not pass, which means you would have to open one of the doors! Of course, if there are no dollar bills left behind a door, you can not open that door!

Let’s play!

Hint: Try to solve this game for (1,2,3) instead of (3,5,7), and you will see that the player who moves first will lose!

To learn about subgame perfect equilibrium, try to explicitly write down the equilibrium strategies in the (1,23) game.

I I have taught game theory and related material for 25+ years and used this game as an example of extensive-form games and subgame perfect equilibrium.

The world has become a lot more affluent over our lifetime. Heck, India has 750,000 millionaires (Dollar millionaires, not rupee millionaires). No matter how you look at it, the stakeholders of large corporations are well-off, thank you. Even if they lose 80% of their annual income , they will still be very well off indeed. This was not the case at any time in history.

So we need to redefine criminal activity for the 21st century.

In the movie “Greed”, the obnoxious super-rich textile tycoon gets fatally mauled by a lion he rented for his own birthday festivities. Well , the mauling episode was facilitated by an young woman employee who “accidentally” pressed the button to open the cage door. It was also witnessed by a resident journalist who was so ” horrified” that he did not call for help , nor report the incident to the cops later.

Are these two people guilty of murder of a horrible human being? The answer is yes!

Since the Roman times where angry and hungry lions were released to prey on slaves for the enjoyment of the spectators, every society frowns on unleashing lions to prey on human beings, no matter how despicable the human being may be. Further , such acts are considered as heinous as first –degree murder and punishable as such.

Consider now a different act. You force a family of three (includes a small child) to live in a small windowless, stuffy room. They can only go outside for twelve hours of backbreaking manual labor every day. You make them eat small, inadequate portions of rice or bread and some basic veggies. The child gets sick but you forbid the parents to seek medical care –she eventually dies. The parents survive ten of fifteen years of your torture and succumb to some common disease because they are very weak.

Are you guilty of murder or abetment to murder? If you do this in USA or in Europe, then you will be guilty of forced labor, torture, imprisonment, child endangerment and a whole bunch of other crimes besides accessory to murder, and will be punished accordingly.

Then why would a multi-national corporation be allowed to pay wages that force people to live like the family described above? Oh yes, to maximize corporate profits! To keep the price of designer jeans and shoes competitive!

F**k that!

I would apply the same criterion as in advanced countries and declare these wages “criminal” wages.

How much wage is considered non-criminal? Well, I have an Econ Ph.D. , so do a lot of others, we will gladly calculate the minimum non-criminal wage for every country and share the information with others.

It is time to change the laws!

The fact that in poor countries employers pay low wages to local workers , does not matter in the 21st century! There are Masai tribes in Kenya who willingly live in areas infested by lions and sometimes get mauled by them, yet releasing a lion to maul humans in a developed society remains a capital offense.

What about labor economics 101 – one uniform wage in a competitive labor market! Well, violating that for a rise in social welfare is not such a big deal. Will this have a serious effect on indigenous enterprises? Since the number of multi-national factories is still relatively small in each Asian or African country, having a dual wage rate is not going to be seriously disruptive.

Yes it will increase the price of consumer goods in the Western societies by about 20 to 25% at the most, but it is a small price to pay to stop people from being murdered, isn’t it?

If anything, it will also shame some new millionaires in India into paying a non-criminal wage to their employees!!